Planning for retirement includes a cornucopia of facts, details and speculation—when do you want to retire, how much will it cost for the lifestyle you want, how long do you think you’ll live—all important considerations.

The money can come from a long list of possibilities—a 401(k), IRAs, non-retirement investments, and Social Security. Oddly enough, one of the biggest assets is often left out of the equation—your home.

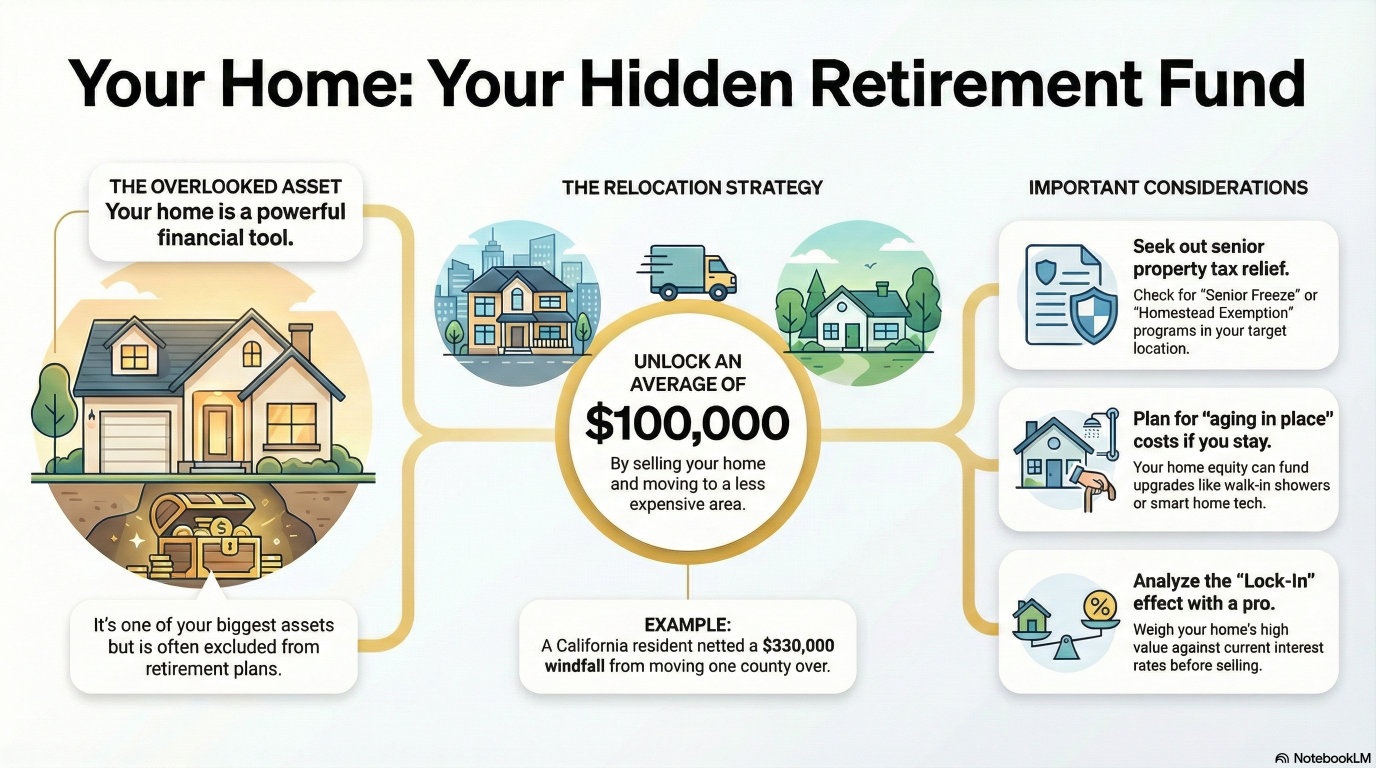

It’s understandable why you might not think of your home as an income resource. You may say, “The house is paid for, so we won’t have to include housing in our retirement budget.” Or your house may have lots of sentimental attachment because you raised your family there and it holds lots of memories. Both are legitimate considerations. But even if you plan to live in your house forever, it’s a good idea to look at it as a part of your retirement treasure chest.

According to a report from Vanguard, the key to unlocking your home’s wealth is something you may not have considered. Vanguard suggests considering relocation to a less expensive real estate market as a possibility.

Now, hold on before you reject the idea of relocating. According to the Vanguard report, by moving to an area with less expensive home prices, the typical American, on average, nets, $100,000 from the move. That means, they sold their existing home, paid cash for one where they relocated, and had $100,000 left over that can be applied to fundng retirement. Moving out of expensive cities could mean you’ll net even more. And in areas of the country where housing prices are much less expensive, the cost of living is usually lower, too.

The Vanguard study gave the example of a 65-year-old resident of Santa Clara, California, selling the average-priced home in that county and buying an average-priced home in Merced County California. That swap netted about $330,000 that could be put toward retirement, assuming no mortgages are involved. And relocating doesn’t necessarily mean you have to move across the country. In the case above, the move was just one county over.

Things to Consider for 2026

Since the world changes fast, here are a few tips for your potential retirement move:

- Property Tax Relief: Many states now offer special tax breaks for seniors. Before you move, check if your new “dream home” location has a “Senior Freeze” or “Homestead Exemption” to keep your taxes low.

- “Aging in Place” Tech: If you decide to stay in your current home, you might need to spend some money on upgrades, like walk-in showers or smart home systems that keep you safe. Your home equity can help pay for these.

- The “Lock-In” Effect: Since home prices have stayed high, your home is likely worth more than you think. However, interest rates are also different than they used to be. It’s important to talk to a pro to see if selling makes sense for your specific budget.

Is Moving Right for You?

No doubt about it, relocating is a big deal. You have to consider proximity to friends, doctors, family and other amenities. But you don’t always have to move far away to find a better deal. Doing a little “homework” on home prices in nearby towns could lead to a much more comfortable retirement and more money in your pocket. Your home is more than just a place to sleep—it’s a financial tool. Don’t leave it out of your plan.

Disclaimer

This information is presented for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy any investment products. None of the information herein constitutes an investment recommendation, investment advice or an investment outlook. The opinions and conclusions contained in this report are those of the individual expressing those opinions. This information is non-tailored, non-specific information presented without regard for individual investment preferences or risk parameters. Some investments are not suitable for all investors, all investments entail risk and there can be no assurance that any investment strategy will be successful. This information is based on sources believed to be reliable and Alhambra is not responsible for errors, inaccuracies, or omissions of information. For more information contact Alhambra Investment Partners at 1-888-777-0970 or email us at info@alhambrapartners.com.

Stay In Touch